Earning miles can be challenging so letting them expire really shouldn’t be an option. There are plenty of ways to keep your reward accounts open by earning, redeeming, or buying miles. Here are some ways this can be achieved without breaking the bank.

Earning Miles

If you’re not a frequent traveler, you always have the option of earning miles via credit card spending. While co-branded credit cards are the obvious option, bank rewards credit cards are worth considering because they transfer to multiple rewards currencies. So if you want to keep more than one account active, having a single transferable rewards card is a great way to minimize the number of credit cards and expenses from annual fees.

For example, Chase Ultimate Rewards points (earned from Ink Cards, Sapphire Preferred, and Freedom credit cards) can be transferred to Hyatt, United, and Southwest, to name a few. If any of these rewards are close to expiring, all it takes is a 1:1 point transfer from your Ultimate Rewards account to keep your miles alive.

Shopping and Surveys

Another option is using online shopping portals. Nearly every major hotel and airline rewards program has a shopping portal that pays out 1 to 10 points per $1 when you shop with popular online merchants.

If you want an even easier option, sign up for a dining rewards program. This requires that you register a credit card with the program of your choice, and anytime you dine at a participating restaurant and use a linked card you will earn miles. You can join them all if you want, though you can’t register the same credit card with more than one program.

Survey sites like e-Rewards and e-Miles are another way to keep your mileage balance active. It takes a large number of surveys to earn enough for a mileage redemption, but they’re relatively easy to earn.

Redeeming Miles

Cashing in some of your miles for a ticket is another way to keep an account active. Some people stockpile their miles without any real goals for redemption. This is a bad strategy — not just because these miles will expire if you don’t continue earning them, but they may devalue at any time without warning. Even redeeming them for magazine subscriptions is preferable to letting miles expire.

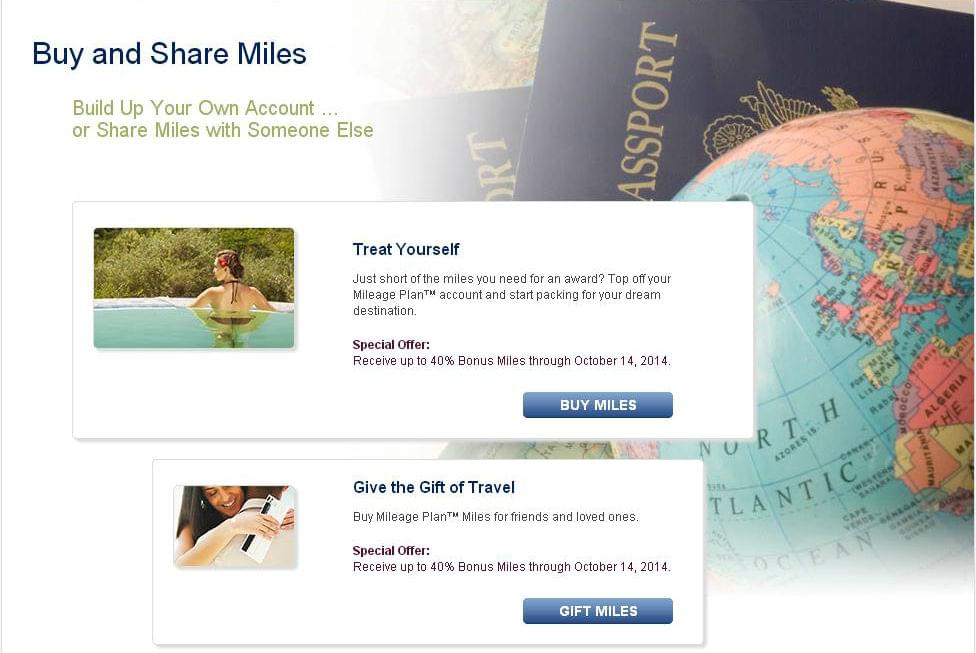

Buying Miles

This is an absolute last resort and only worth considering if you stand to lose a large balance and the above methods aren’t an option.

Sometimes rewards programs run generous sales on the purchase of miles. I’m personally not a fan of this and wouldn’t advocate buying them in large quantities. I don’t care that $1,900 buys enough miles for a business-class trip to Asia. If you’re not in a position to pay that much for an economy ticket, you shouldn’t think of it as a “good deal just because it’s in business class.

Sticking to your budget is more important than getting 20 likes on Instagram when you post a photo of your fancy seat. If you’re going to buy miles, buy the minimum to keep your account active, but only as a last resort.

Next: Which programs have points or miles that don’t expire.