When an entrepreneur first starts a business, cash flow is crucial. Many will get loans to fund the initial effort. Some will seek out help from family and friends. Others will turn to credit cards as a way to pay for the expenses that come with a new business. There are some common myths about using

You Need an EIN to Apply for a Business Credit Card

One of the most widespread business credit card myths is that you need to be a corporation to be approved. The truth is that anyone can apply for a business credit card, even if you don’t own a traditional business with an EIN number. Instead you can apply as a sole proprietor.

The IRS defines a sole proprietor as “someone who owns an unincorporated business by himself or herself.” Maybe you sell items on ebay, operate a small lawn care business or act as a consultant. If you are earning revenue, then you are a business owner in the eyes of the IRS.

If you are a sole proprietor applying for a business credit card, you would use your legal name as the business name and your social security number would be your tax ID number.

One thing to know before applying for a business credit card is that certain issuers will report activity to consumer credit bureaus. You might be asking yourself why they would do this. The answer is because they want to have a personal guarantee that you are going to pay back the money you borrow. If you would prefer to to keep your personal credit out of the equation, then consider a card from Bank of America, Citi, or Wells Fargo. Chase, American Express and US Bank are other options because they will only report negative information to consumer credit bureaus.

Employee Cards Can Be Expensive

One of the nice things about having a credit card for your business is that your employees can have cards on the same account. If you have a rewards card then this can help increase the amount of rewards you can potentially earn each month.

However, some people believe that employee cards will end up costing the business more money. While there are certain cards that have a fairly steep annual fee for employee cards, there are a bunch that are completely free. If you’d like to provide your employees with company cards, then consider one of the following credit cards.

- Chase Ink Business Cash Card

- Chase Business Preferred Card

- Amex SimplyCash Plus Business Card

- Business Gold Rewards Card from American Express ($50 for the first card, $0 for every other card)

You Need Excellent Credit for a Business Credit Card

While it’s true that you need excellent credit to get a majority of the business credit cards available, there are still options. The Capital One Spark Classic for Business card will approve you even with average credit. If your credit is lower than that, you might need to start with a secured card. The Wells Fargo Business Secured card or BBVA Compass Business Secured Card are great options.

With a secured business card you will be required to put down a deposit that will act as your credit limit. These cards will help you improve your credit score and eventually move into a credit card that will offer more benefits for your business.

Using Your Personal Credit Card for Business Purchases is Acceptable

When starting a business many entrepreneurs might turn to their personal credit cards first. While this might seem like an easy solution, it can come back to cause problems in the future. If your expenses start getting close to your credit limit, this will push your credit utilization to unfavorable levels. Because this makes up a large piece of your credit score, you would start seeing your scores drop. This could also affect your ability to obtain additional financing in the future.

Applying for a business credit card will keep this from happening. As we mentioned earlier, only select issuers will report any activity from a business card to consumer credit bureaus. As long as you don’t default on your account, you should be able to keep everything separate.

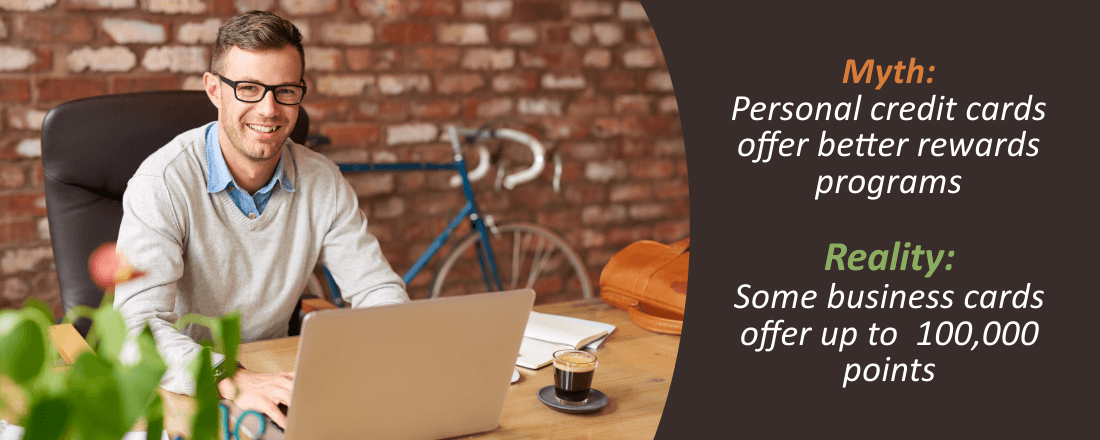

Personal Credit Cards Will Offer More Attractive Rewards

It’s no secret that there are a lot of personal credit cards offering very attractive rewards. Many people feel these rewards are better than what business cards can offer. This is actually the opposite from the truth. There are cards that offer $500 and even cards that offer up to 100,000 points after meeting spending requirements.

Where business credit cards really differentiate themselves from personal cards is with purchases rewards. Many personal cards have rather low limits on purchases that can earn a bonus. The Chase Freedom card has a limit of $1,500 per quarter in combined purchases. However, the Chase Ink Business Preferred card offers bonus points on the first $50,000 each year in select categories.

So why do credit card issuers offer such generous bonuses to businesses? The answer is simple. Businesses are more likely to carry debt from one month to the next, which means a greater profit.

No Pre-set Spending Limit Credit Cards Actually Have Limits

If you’ve never heard of no pre-set spending limit credit cards, you’re probably not alone. These cards sound like they might come without a set credit limit, but they actually do. As an example, let’s consider American Express. Many classic American Express cards, like the Business Platinum card, are not credit cards, they are actually charge cards. Instead of being able to carry a balance from month to month, you are required to pay off your balance at the end of each statement period. That makes it seem like you can charge as much as you want as long as you pay it off. However, this is not the case.

Card issuers will actually set a spending limit for each cardholder based on certain criteria like income, payment history, past spending patterns, etc. But the truth is, no many businesses know how much they might need to spend each month. That means it’s important to make sure you keep your spending in check. If you end up hitting your limit, then there is a chance they could report this behavior to consumer credit bureaus.

For anyone just getting a business off the ground, a business credit card can be a big help. It’ll provide you with the liquidity you need to enable growth. Just be aware of how your credit card works. By not understanding the way business cards operate, you could be risking your business and your personal credit score.